If you’re thinking of buying a home, chances are you’re paying attention to just about everything you hear about the housing market. And you’re getting your information from a variety of channels: the news, social media, your real estate agent, conversations with friends and loved ones, overhearing someone chatting at the local supermarket, the list goes on and on. Most likely, home prices and mortgage rates are coming up a lot.

To help cut through the noise and give you the information you need most, take a look at what the data says. Here are the top two questions you need to ask yourself about home prices and mortgage rates as you make your decision:

One reliable place you can turn to for that information is the Home Price Expectation Survey from Pulsenomics – a survey of a national panel of over one hundred economists, real estate experts, and investment and market strategists.

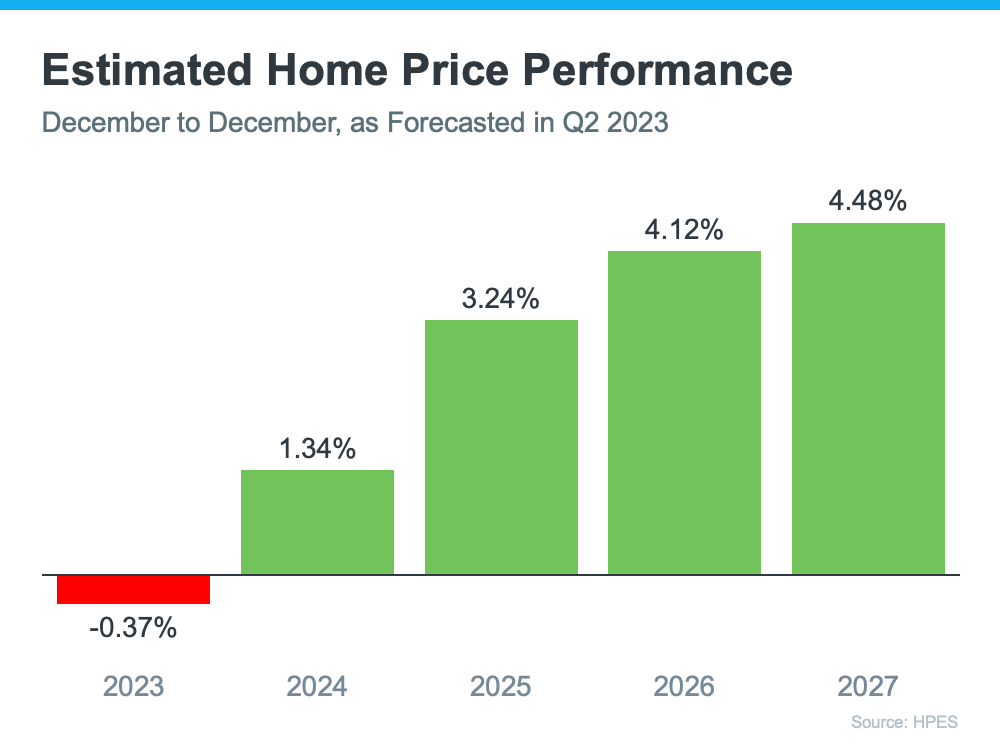

According to the latest release, the experts surveyed are projecting slight depreciation this year (see the red in the graph below). But here’s the context you need most. The worst home price declines are already behind us, and prices are actually appreciating again in many markets. Not to mention, the small 0.37% depreciation HPES is showing for 2023 is far from the crash some people originally said would happen.

Now, let’s look to the future. The green in the graph below shows prices have turned a corner and are expected to appreciate in 2024 and beyond. After this year, the HPES is forecasting home price appreciation returning to more normal levels for the next several years.

So, why does this matter to you? It means your home will likely grow in value and you should gain home equity in the years ahead, but only if you buy now. If you wait, based on these forecasts, the home will only cost you more later on.

Over the past year, mortgage rates have risen in response to economic uncertainty, inflation, and more. We know based on the latest reports that inflation, while still high, has moderated from its peak. This is an encouraging sign for the market and for mortgage rates. Here’s why.

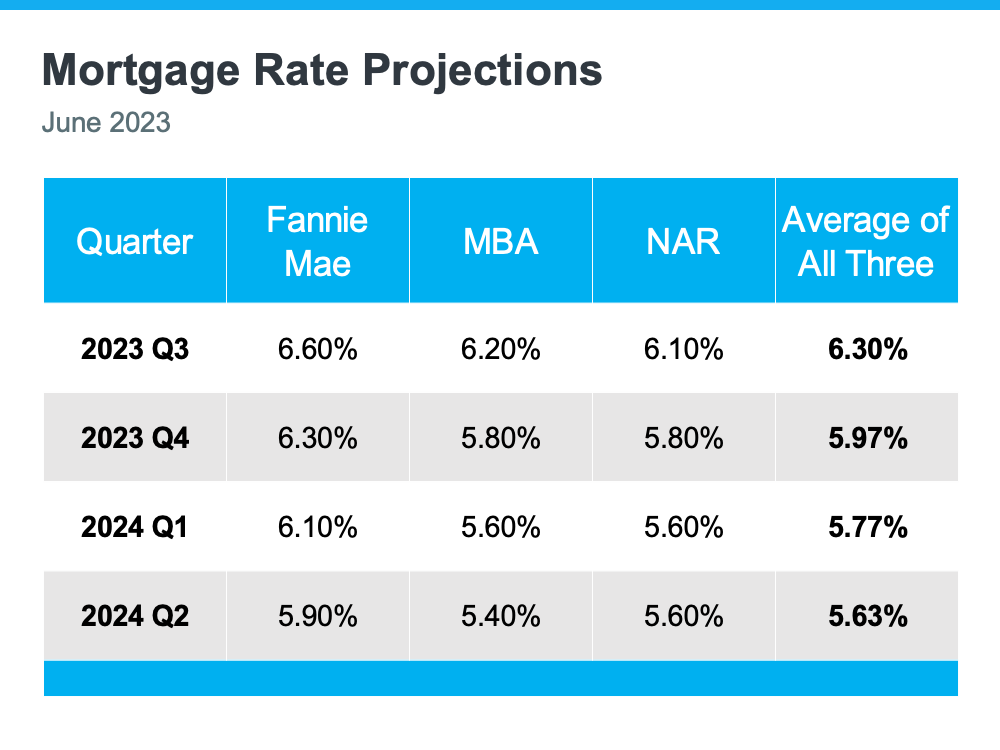

When inflation cools, mortgage rates generally fall in response. This may be why some experts are saying mortgage rates will pull back slightly over the next few quarters and settle somewhere around roughly 5.5 and 6% on average.

But, not even the experts can say with absolute certainty where mortgage rates will be next year, or even next month. That’s because there are so many factors that can impact what happens. So, to give you a lens into the various possible outcomes, here’s what you should consider:

Bottom Line

If you’re thinking about buying a home, you need to know the facts on what’s happening with home prices and mortgage rates. While no one can say for certain where they’ll go, expert projections can give you powerful information to keep you informed. Let’s connect so you have a professional to add in an expert opinion on our local market.

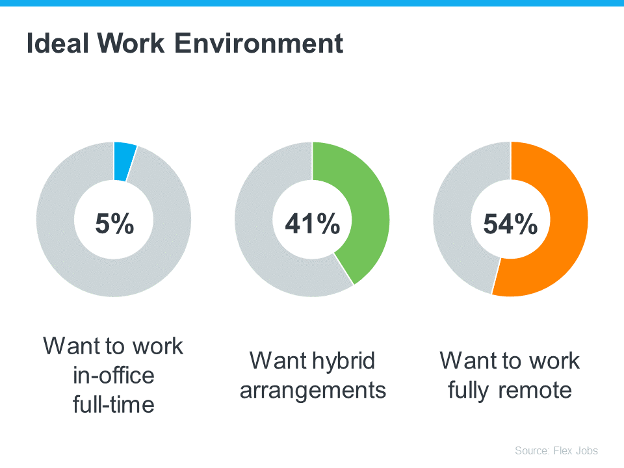

Even as some companies transition back into the office, remote work remains a popular choice for many professionals. So, if you enjoy working from home or hope to be able to soon, you’re not alone. According to a recent survey, most working professionals want to

work either fully remote or hybrid (see below):

This trend is good news if you’re looking to buy a home because a remote or hybrid work setup can help you overcome some of today’s affordability and housing inventory challenges.

More Work Flexibility Equals More Home Options

Remote or hybrid work opens up a world of opportunities. That’s because it allows you to broaden your search for your next home since you’re no longer limited to living close to your workplace. With the freedom to work from anywhere, you can explore more affordable areas that may be located farther away from bustling city centers or your office. This flexibility can be a game changer while higher mortgage rates are making it difficult for some homebuyers to afford a home.

An article from the New York Times (NYT) highlights how remote work can greatly assist you in overcoming that challenge:

“. . . take advantage of the opportunity remote work has presented to move to more affordable communities (either farther out in the suburbs, or in another part of the country).”

And, since the supply of homes for sale is still so low, another key challenge for you today may be finding something with all of the features you want and need. Because remote work allows you to broaden your search radius to include additional areas, you may actually have less trouble finding a home with the features you want the most because you’ll have a bigger pool of options to pick from.

Working remotely gives you the flexibility to find an affordable home with the features you want. In other words, you have a better chance of getting what you need without blowing your budget.

Bottom Line

Working remotely not only gives you more flexibility in your job but also presents a great chance to broaden your search for a home. Since you’re not limited to a specific location, you have the opportunity to explore more options. Let’s get in touch to discuss how this can expand your choices and help you find the perfect home.

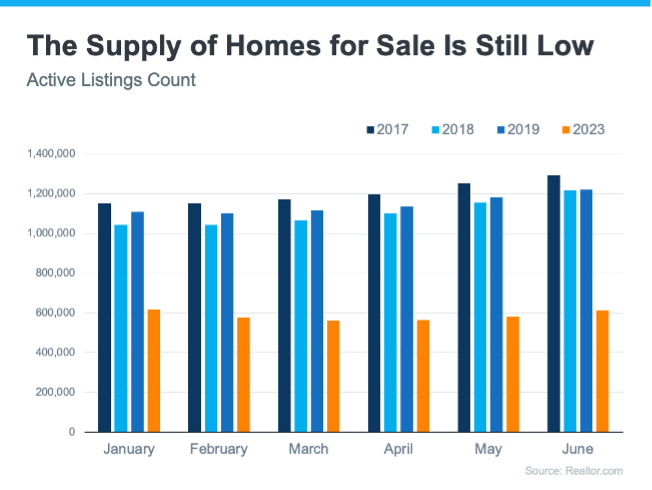

One of the biggest challenges in the housing market right now is how few homes there are for sale compared to the number of people who want to buy them. To help emphasize just how limited housing inventory still is, let’s take a look at the latest information on active listings, or homes for sale in a given month, as it compares to more normal levels.

According to a recent report from Realtor.com:

“On average, active inventory in June was 50.6% below pre-pandemic 2017–2019 levels.”

The graph below helps illustrate this point. It uses historical data to provide a more concrete look at how much the numbers are still lagging behind the level of inventory typical of a more normal market :

It’s worth noting that 2020-2022 are not included in this graph. That’s because they were truly abnormal years for the housing market. To make the comparison fair, those have been omitted so they don’t distort the data.

When you compare the orange bars for 2023 with the last normal years for the housing market (2017-2019), you can see the count of active listings is still far below the norm.

What Does This Mean for You?

If you’re thinking about selling your house, that low inventory is why this is a great time to do so. Buyers have fewer choices now than they did in more normal years, and that’s continuing to impact some key statistics in the housing market. For example, sellers will be happy to see the following data from the latest Confidence Index from the National Association of Realtors (NAR):

Bottom Line

When supply is so low, your house is going to be in the spotlight. That’s why sellers are seeing their homes sell a little faster an

d get more offers right now. If you’ve thought about selling, now’s the time to make a move. Let’s connect to get the process started.

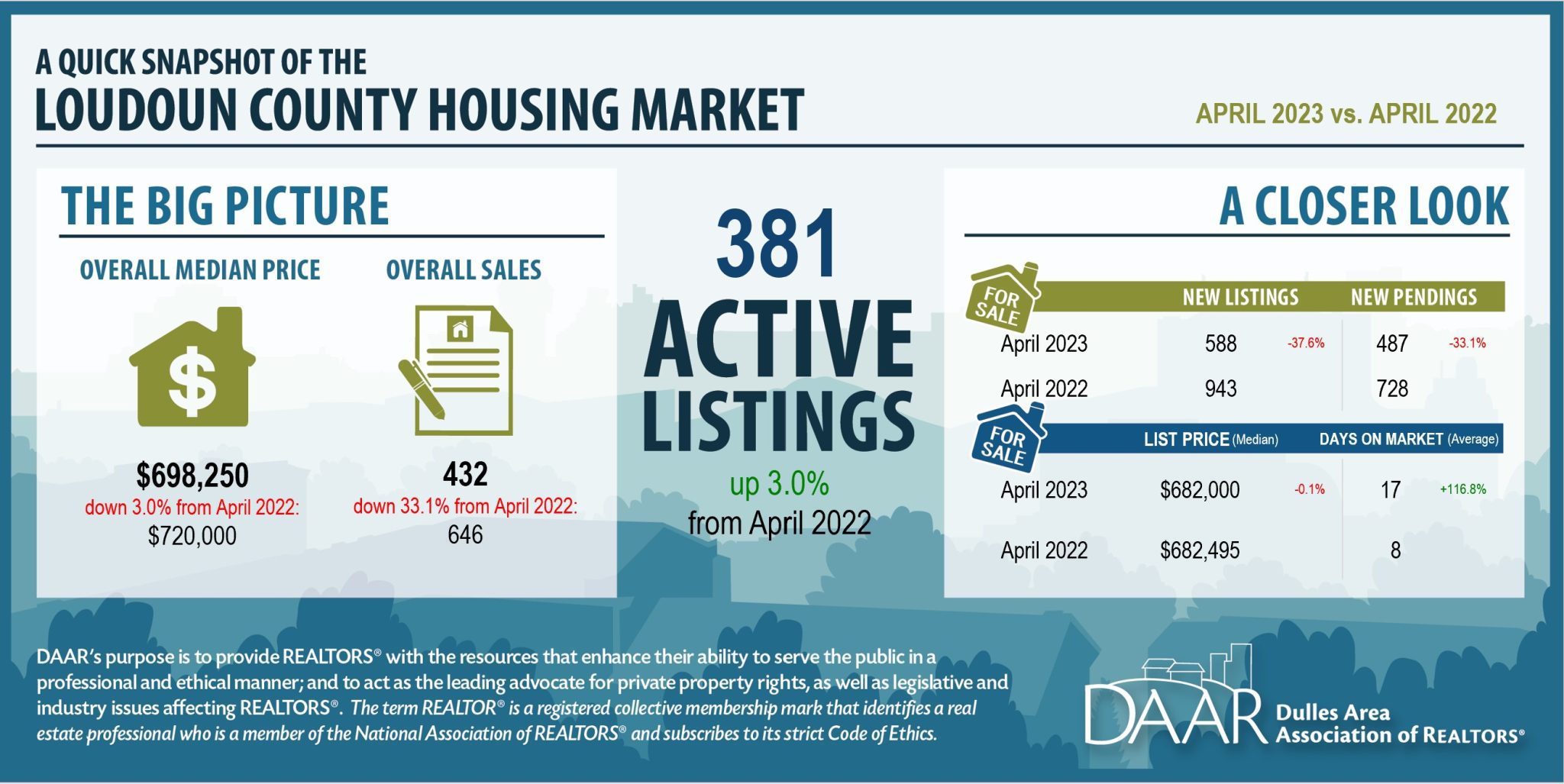

Key Market Trends

Sales activity remains well below last year’s level across most local markets in Loudoun County.

There were 432 sales countywide this month, 214 fewer sales than last April, a 33.1% drop off in activity. This is the slowest April market the county has had in more than a decade. Ashburn zip code 20148 had the biggest decrease in sales with 33 fewer sales than last year (-30.8%) while sales in Leesburg zip code 20176 declined by 21 sales (-29.2%). The only market where sales increased was Lovettsville 20180 with seven more sales than the previous year (+63.6%).

Pending sales cool, signaling a continuation of the slow spring market.

There were 487 pending sales in April in Loudoun County, 241 fewer pending sales than the same time a year ago, falling by 33.1%. Pending sales dipped the most in Ashburn zip code 20147 with 41 fewer pending sales (-34.2%) and Aldie zip code 20105 with 35 fewer pending sales than last year (-51.5%).

The median sales price in the Loudoun County housing market dipped from last April.

In April, the median sales price countywide was $698,250, a 3% decrease in price, which is $21,750 less than last year. This is only the second time in the last four years that the monthly median sales price was lower than the prior year. The sharpest price drops occurred in Lovettsville zip code 20180 down $135,000 from a year ago (-16.3%), Leesburg zip code 20175 (-12.2%) and Chantilly zip code 20152 (-11.1%). In Aldie zip code 20105, home prices were up $45,000 or 5.4%.

The number of active listings continues to build up in most parts of the county.

There were 381 active listings at the end of April in Loudoun County, 11 more listings than the year prior, a 3% increase. In Sterling zip code 20164 there were 13 more listings on the market than last year (+56.5%). Listings fell in Chantilly zip code 20152 with nine fewer listings than the previous year (-52.9%). The total number of new listings in Loudoun County plunged by 37.6% compared to last April.

Data Note: The housing market data for all jurisdictions in Virginia was re-benchmarked in November 2021. Please note that Market Indicator Reports released prior to November 2021 were produced using the prior data vintage and may not tie to reports that use the current data set for some metrics. We recommend using the current reports for historical comparative analysis.

If you’re reading headlines about inflation or mortgage rates, you may see something about the recent decision from the Federal Reserve (the Fed). But what does it mean for you, the housing market, and your plans to buy a home? Here’s what you need to know.

Inflation and the Housing Market

While the Fed’s working hard to lower inflation, the latest data shows that, while the number has improved some, the inflation rate is still higher than the target (2%). That played a role in the Fed’s decision to raise the Federal Funds Rate last week. As Bankrate explains:

“Keeping its inflation-fighting streak alive, the Federal Reserve has raised interest rates for the 10th time in 10 meetings . . . The hikes aimed to cool an economy that was on fire after rebounding from the coronavirus recession of 2020.”

While the Fed’s actions don’t directly dictate what happens with mortgage rates, their decisions do have an impact and contributed to the intentional cooldown in the housing market last year.

How This Impacts You

During times of high inflation, your everyday expenses go up. That means you’ve likely felt the pinch at the gas pump and in the grocery store. By raising the Federal Funds Rate, the Fed is actively trying to lower inflation. If the Fed is successful, it could also ultimately lead to lower mortgage rates and better homebuying affordability for you. That’s because when inflation is high, mortgage rates tend to be high. But, as inflation cools, experts say mortgage rates will likely fall.

Where Experts Think Mortgage Rates and Inflation Will Go from Here

Moving forward, both inflation and mortgage rates will continue to impact the housing market. And as Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Mortgage rates are likely to descend lower later in the year as the consumer price inflation calms down . . .”

Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), explains:

“We continue to expect that mortgage rates will drift down over the course of the year as the economy slows . . .”

While there’s no way to say with certainty where mortgage rates will go from here, the experts think mortgage rates will trend down this year if inflation comes down too. To stay informed on the latest insights, connect with a trusted real estate advisor. They keep their pulse on what’s happening today and help you understand what the experts are projecting and how it could impact your homeownership plans.

Bottom Line

Don’t let headlines about the latest decision from the Fed confuse you. Where mortgage rates go from here depends on what happens with inflation. If inflation cools, mortgage rates should tick down as a result. Let’s connect so you have expert insights on housing market changes and what they mean for you.

How Bridge Loans Can Help You Purchase

Bridge loans are a great financial tool to provide you

with the flexibility to make a non-contingent offer, leverage the equity in

your current home without having to do a simultaneous close/move, and/or

qualify for a purchase prior to selling your departing property.

The most common type of bridge loan is a current (departing)

property bridge loan which pulls equity out of your current primary residence

to be used for the down payment on a new home or to purchase your new home in

cash.

A bridge loan can also be used on the property you are purchasing.

One benefit of a purchase bridge loan is that if certain conditions are met

(departing residence listed for sale and available reserves) then the monthly

payment associated with the departing residence may be excluded from the DTI calculation.

This allows a borrower who doesn’t qualify carrying both homes

to purchase their new home prior to selling their departing residence.

A bridge loan can be used on both the departing residence

and the purchase property when the borrower needs both the equity from the

current property yet does not qualify carrying both properties.

Atlantic Coast Mortgage bridge loans are 6-month interest only with no

escrows and are allowed on primary residences or second homes in DC, MD, NC,

VA, and Charleston, SC MSA. The bridge loan will take first lien position so any existing mortgages will be paid off in addition any proceeds received.

For further information please reach out to Melissa Bell, NMLS ID 450558, with Atlantic Coast Mortgage.

Atlantic Coast Mortgage, LLC is an Equal Housing Lender

Everywhere you look, people are talking about a potential recession. And if you’re planning to buy or sell a house, this may leave you wondering if your plans are still a wise move. To help ease your mind, experts are saying that if we do officially enter a recession, it’ll be mild and short. As the Federal Reserve explained in their March meeting:

“. . . the staff’s projection at the time of the March meeting included a mild recession starting later this year, with a recovery over the subsequent two years.”

While a recession may be on the horizon, it won’t be one for the housing market record books like the crash in 2008. What we have to remember is that a recession doesn’t always lead to a housing crisis.

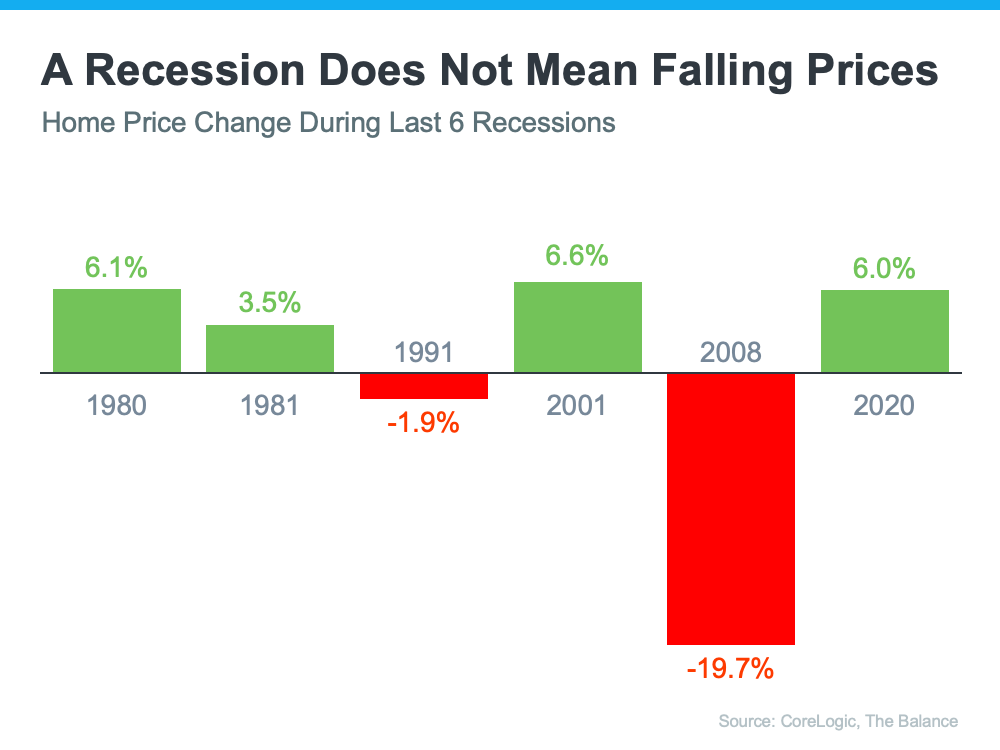

To prove it, let’s look at the historical data of what happened in real estate during previous recessions. That way you know why you shouldn’t be afraid of what a recession could mean for the housing market today.

A Recession Doesn’t Mean Falling Home Prices

To show that home prices don’t fall every time there’s a recession, it helps to turn to historical data. As the graph below illustrates, looking at recessions going all the way back to 1980, home prices appreciated in four of the last six of them. So historically, when the economy slows down, it doesn’t mean home values will always fall.

Most people remember the housing crisis in 2008 (the larger of the two red bars in the graph above) and think another recession will be a repeat of what happened to housing then. But today’s housing market isn’t about to crash because the fundamentals of the market are different than they were in 2008. Back then, one of the big reasons why prices fell was because there was a surplus of homes for sale at the same time distressed properties flooded the market. Today, the number of homes for sale is low, so while home prices may see slight declines in some areas and slight gains in others, a crash simply isn’t in the cards.

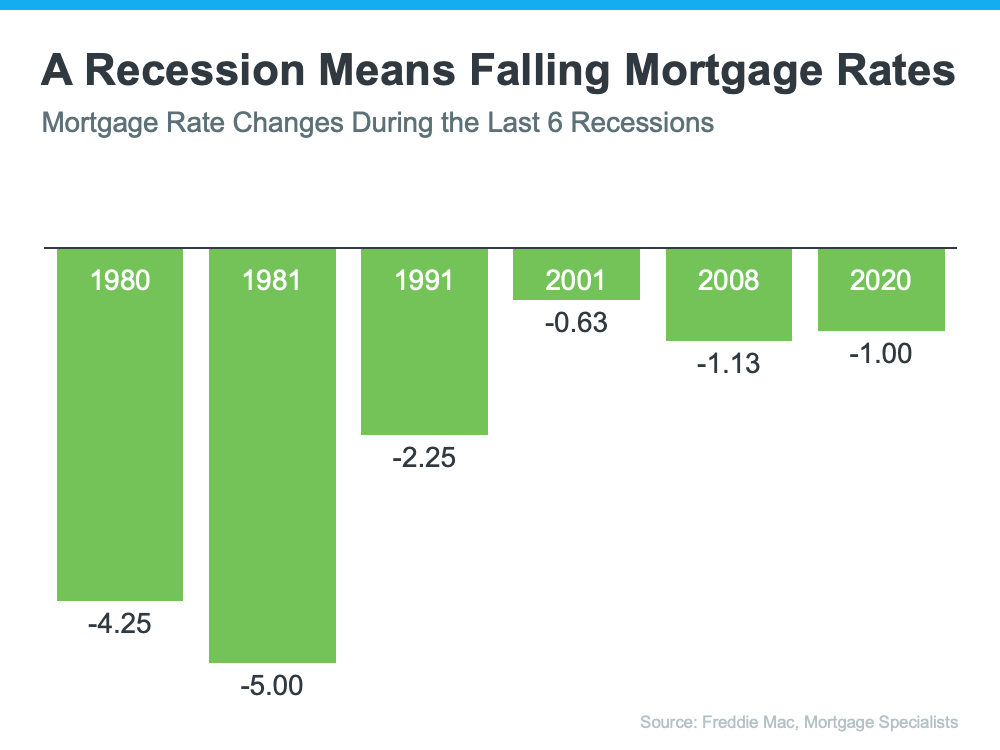

A Recession Means Falling Mortgage Rates

What a recession really means for the housing market is falling mortgage rates. As the graph below shows, historically, each time the economy slowed down, mortgage rates decreased.