If you’re thinking of buying a home, chances are you’re paying attention to just about everything you hear about the housing market. And you’re getting your information from a variety of channels: the news, social media, your real estate agent, conversations with friends and loved ones, overhearing someone chatting at the local supermarket, the list goes on and on. Most likely, home prices and mortgage rates are coming up a lot.

To help cut through the noise and give you the information you need most, take a look at what the data says. Here are the top two questions you need to ask yourself about home prices and mortgage rates as you make your decision:

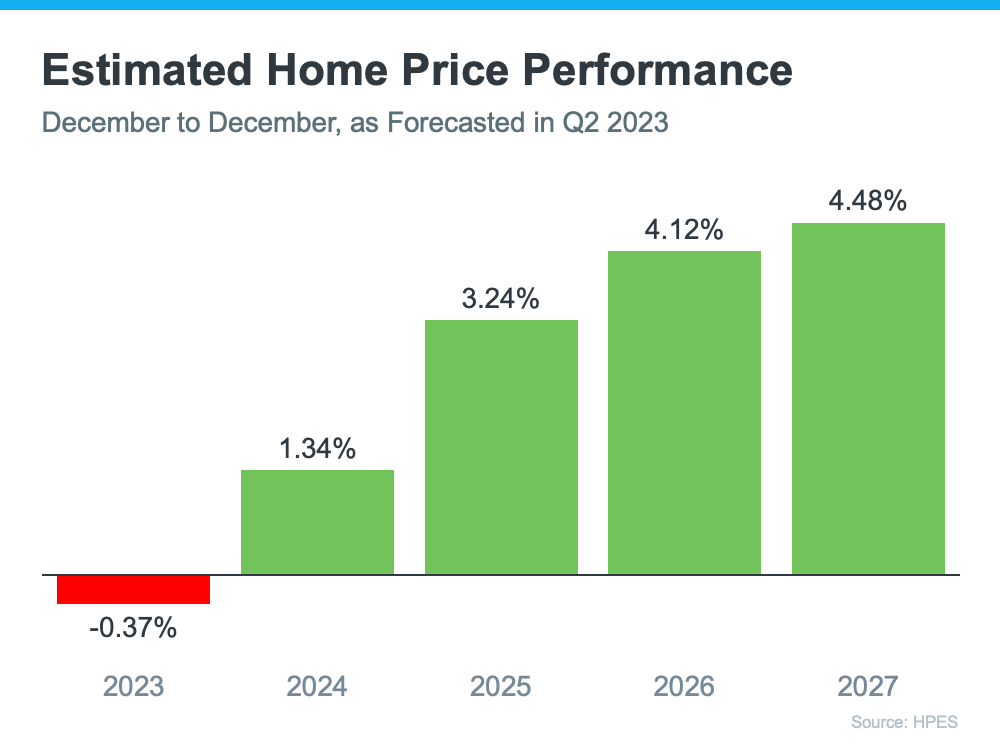

One reliable place you can turn to for that information is the Home Price Expectation Survey from Pulsenomics – a survey of a national panel of over one hundred economists, real estate experts, and investment and market strategists.

According to the latest release, the experts surveyed are projecting slight depreciation this year (see the red in the graph below). But here’s the context you need most. The worst home price declines are already behind us, and prices are actually appreciating again in many markets. Not to mention, the small 0.37% depreciation HPES is showing for 2023 is far from the crash some people originally said would happen.

Now, let’s look to the future. The green in the graph below shows prices have turned a corner and are expected to appreciate in 2024 and beyond. After this year, the HPES is forecasting home price appreciation returning to more normal levels for the next several years.

So, why does this matter to you? It means your home will likely grow in value and you should gain home equity in the years ahead, but only if you buy now. If you wait, based on these forecasts, the home will only cost you more later on.

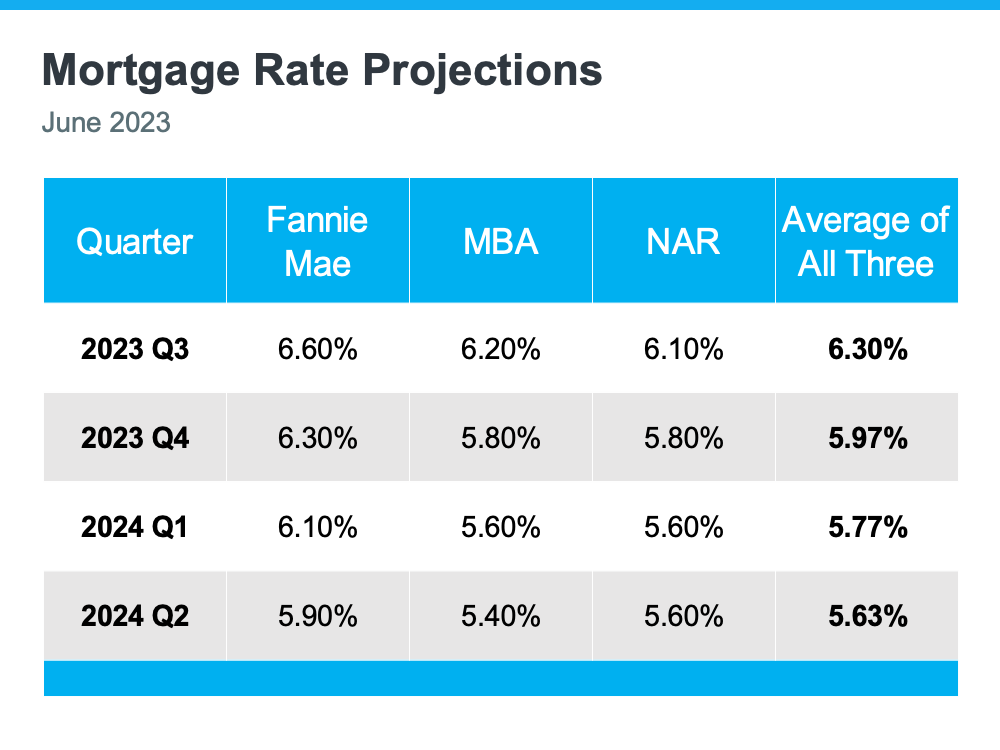

Over the past year, mortgage rates have risen in response to economic uncertainty, inflation, and more. We know based on the latest reports that inflation, while still high, has moderated from its peak. This is an encouraging sign for the market and for mortgage rates. Here’s why.

When inflation cools, mortgage rates generally fall in response. This may be why some experts are saying mortgage rates will pull back slightly over the next few quarters and settle somewhere around roughly 5.5 and 6% on average.

But, not even the experts can say with absolute certainty where mortgage rates will be next year, or even next month. That’s because there are so many factors that can impact what happens. So, to give you a lens into the various possible outcomes, here’s what you should consider:

Bottom Line

If you’re thinking about buying a home, you need to know the facts on what’s happening with home prices and mortgage rates. While no one can say for certain where they’ll go, expert projections can give you powerful information to keep you informed. Let’s connect so you have a professional to add in an expert opinion on our local market.

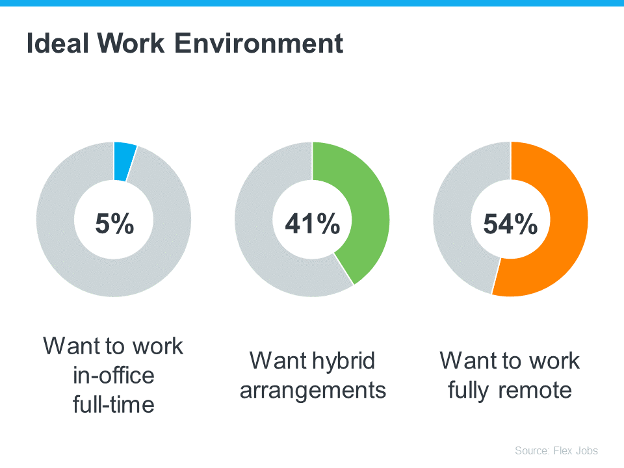

Even as some companies transition back into the office, remote work remains a popular choice for many professionals. So, if you enjoy working from home or hope to be able to soon, you’re not alone. According to a recent survey, most working professionals want to

work either fully remote or hybrid (see below):

This trend is good news if you’re looking to buy a home because a remote or hybrid work setup can help you overcome some of today’s affordability and housing inventory challenges.

More Work Flexibility Equals More Home Options

Remote or hybrid work opens up a world of opportunities. That’s because it allows you to broaden your search for your next home since you’re no longer limited to living close to your workplace. With the freedom to work from anywhere, you can explore more affordable areas that may be located farther away from bustling city centers or your office. This flexibility can be a game changer while higher mortgage rates are making it difficult for some homebuyers to afford a home.

An article from the New York Times (NYT) highlights how remote work can greatly assist you in overcoming that challenge:

“. . . take advantage of the opportunity remote work has presented to move to more affordable communities (either farther out in the suburbs, or in another part of the country).”

And, since the supply of homes for sale is still so low, another key challenge for you today may be finding something with all of the features you want and need. Because remote work allows you to broaden your search radius to include additional areas, you may actually have less trouble finding a home with the features you want the most because you’ll have a bigger pool of options to pick from.

Working remotely gives you the flexibility to find an affordable home with the features you want. In other words, you have a better chance of getting what you need without blowing your budget.

Bottom Line

Working remotely not only gives you more flexibility in your job but also presents a great chance to broaden your search for a home. Since you’re not limited to a specific location, you have the opportunity to explore more options. Let’s get in touch to discuss how this can expand your choices and help you find the perfect home.

How Bridge Loans Can Help You Purchase

Bridge loans are a great financial tool to provide you

with the flexibility to make a non-contingent offer, leverage the equity in

your current home without having to do a simultaneous close/move, and/or

qualify for a purchase prior to selling your departing property.

The most common type of bridge loan is a current (departing)

property bridge loan which pulls equity out of your current primary residence

to be used for the down payment on a new home or to purchase your new home in

cash.

A bridge loan can also be used on the property you are purchasing.

One benefit of a purchase bridge loan is that if certain conditions are met

(departing residence listed for sale and available reserves) then the monthly

payment associated with the departing residence may be excluded from the DTI calculation.

This allows a borrower who doesn’t qualify carrying both homes

to purchase their new home prior to selling their departing residence.

A bridge loan can be used on both the departing residence

and the purchase property when the borrower needs both the equity from the

current property yet does not qualify carrying both properties.

Atlantic Coast Mortgage bridge loans are 6-month interest only with no

escrows and are allowed on primary residences or second homes in DC, MD, NC,

VA, and Charleston, SC MSA. The bridge loan will take first lien position so any existing mortgages will be paid off in addition any proceeds received.

For further information please reach out to Melissa Bell, NMLS ID 450558, with Atlantic Coast Mortgage.

Atlantic Coast Mortgage, LLC is an Equal Housing Lender

The Power of Pre-Approval

If you’re buying a home this spring, today’s housing market can feel like a challenge. With so few homes on the market right now, plus higher mortgage rates, it’s essential to have a firm grasp on your homebuying budget. You’ll also need a sense of determination to find the right house and act quickly when you go to put in an offer. One thing you can do to help you prepare is to get pre-approved.

To understand why it’s such an important step, you need to know what pre-approval is. As part of the process, a lender looks at your finances to determine what they’d be willing to loan you. From there, your lender will give you a pre-approval letter to help you understand how much money you can borrow.

Freddie Mac explains it like this:

“A pre-approval is an indication from your lender that they are willing to lend you a certain amount of money to buy your future home. . . . Keep in mind that the loan amount in the pre-approval letter is the lender’s maximum offer. Ultimately, you should only borrow an amount you are comfortable repaying.”

Basically, pre-approval gives you critical information about the homebuying process that’ll help you understand how much you may be able to borrow so you have a stronger grasp of your options. And with higher mortgage rates impacting affordability for many buyers today, a solid understanding of your numbers is even more important.

Pre-Approval Helps Show You’re a Serious Buyer

That’s not the only thing pre-approval can do. Another added benefit is it can help a seller feel more confident in your offer because it shows you’re serious about buying their house. And, with sellers seeing a slight increase in the number of offers again this spring, making a strong offer when you find the perfect house is key.

As a recent article from the Wall Street Journal (WSJ) says:

“If you plan to use a mortgage for your home purchase, preapproval should be among the first steps in your search process. Not only can getting preapproved help you zero in on the right price range, but it can give you a leg up on other buyers, too.”

Bottom Line

Getting pre-approved is an important first step when you’re buying a home. It lets you know what you can borrow for your loan and shows sellers you’re serious. Connect with a local real estate professional and a trusted lender so you have the tools you need to purchase a home in today’s market.

As the housing market continues to change, you may be wondering where it’ll go from here. One factor you’re probably thinking about is home prices, which have come down a bit since they peaked last June. And you’ve likely heard something in the news or on social media about a price crash on the horizon. As a result, you may be holding off on buying a home until prices drop significantly. But that’s not the best strategy.

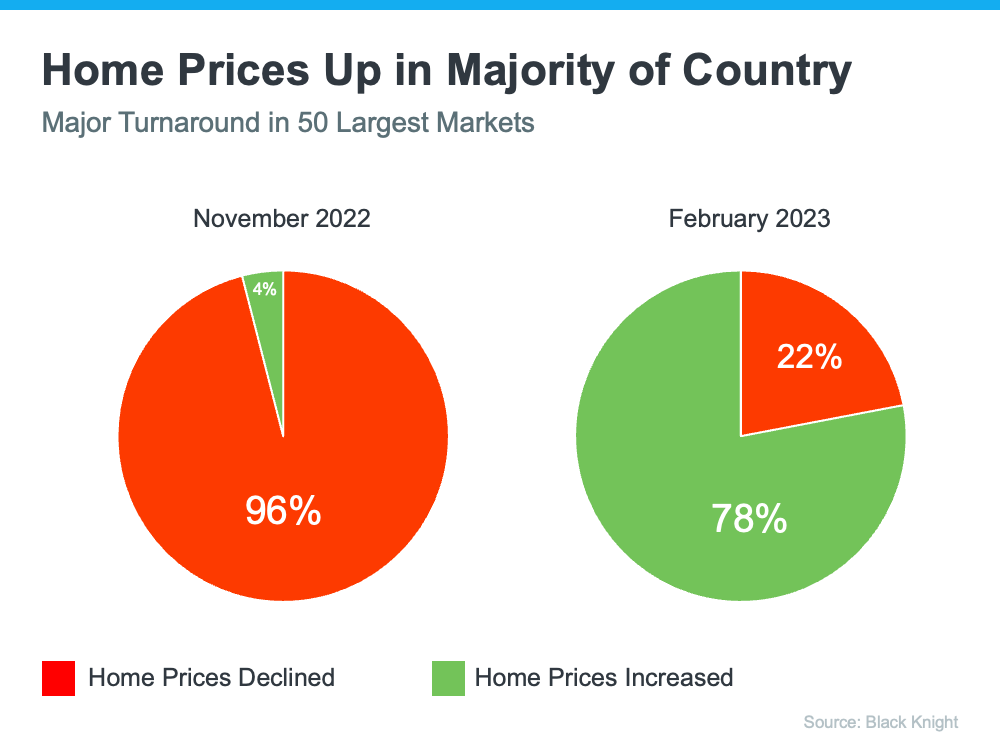

A recent survey from Zonda shows 53% of millennials are still renting right now because they’re waiting for home prices to come down. But here’s the thing: the most recent data shows that home prices appear to have bottomed out and are now on the rise again. Selma Hepp, Chief Economist at CoreLogic, reports:

“U.S. home prices rose by 0.8% in February . . . indicating that prices in most markets have already bottomed out.”

And the latest data from Black Knight shows the same shift. The graph below compares home price trends in November to those in February:

Thinking about selling your house? If you’ve been waiting for the right time, it could be now while the supply of homes for sale is so low. HousingWire shares:

“. . . the big question is whether we are finally starting to see the seasonal spring increase in inventory. The answer is no, because active listings fell to a new low last week for 2023 . . .”

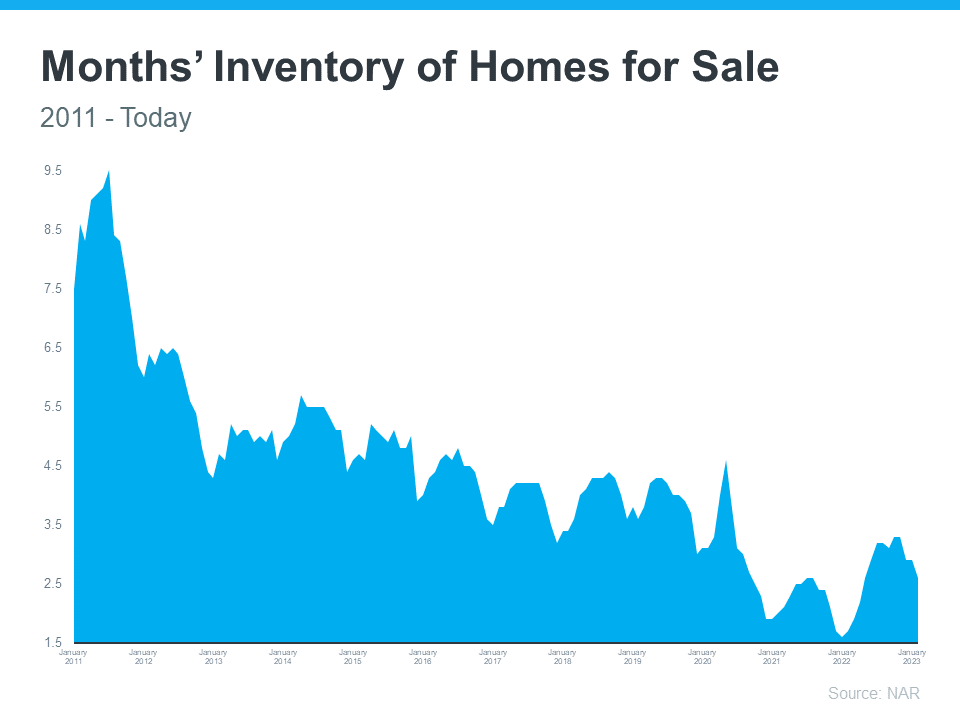

The National Association of Realtors (NAR) confirms today’s housing inventory is low by looking at the months’ supply of homes on the market. In a balanced market, about a six-month supply is needed. Anything lower is a sellers’ market. And today, the number is much lower:

“Total housing inventory registered at the end of February was 980,000 units, identical to January and up 15.3% from one year ago (850,000). Unsold inventory sits at a 2.6-month supply at the current sales pace, down 10.3% from January but up from 1.7 months in February 2022.”

Why Does Low Inventory Make It a Good Time To Sell?

The less inventory there is on the market when you sell, the less competition you’re likely to face from other sellers. That means your house will get more attention from the buyers looking for a home this spring. And since there are significantly more buyers in the market than there are homes for sale, you could even receive more than one offer on your house. Multiple offers are on the rise again (see graph below):

That lack of available homes on the market is putting upward pressure on prices. Bankrate puts it like this:

“This ongoing lack of inventory explains why many buyers still have little choice but to bid up prices. And it also indicates that the supply-and-demand equation simply won’t allow a price crash in the near future.”

There have been a lot of shifts in the housing market recently. Mortgage rates rose dramatically last year, impacting many people’s ability to buy a home. And after several years of rapid price appreciation, home prices finally peaked last summer. These changes led to a rise in headlines saying prices would end up crashing.

Even though we’re no longer seeing the buyer frenzy that drove home values up during the pandemic, prices have been relatively flat at the national level. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), doesn’t expect that to change:

“[H]ome prices will be steady in most parts of the country with a minor change in the national median home price.”

You might think sellers would have to lower prices to attract buyers in today’s market, and that’s part of why some may have been waiting for prices to come crashing down. But there’s another factor at play – low inventory. And according to Yun, that’s limiting just how low prices will go:

“We simply don’t have enough inventory. Will some markets see a price decline? Yes. [But] with the supply not being there, the repeat of a 30 percent price decline is highly, highly unlikely.”

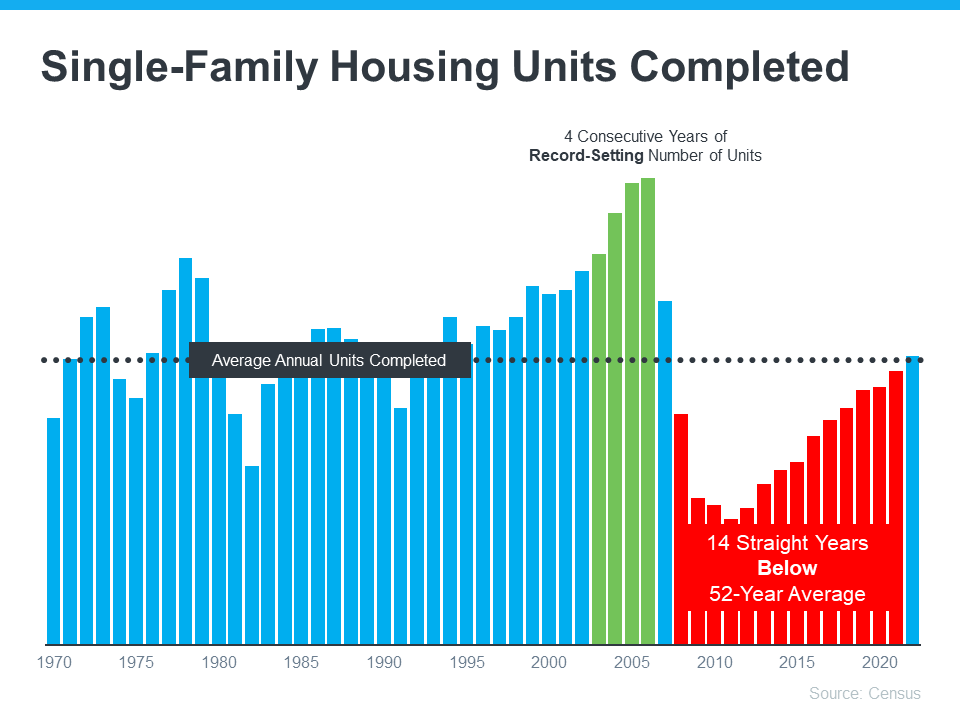

As you can see in the graph below, we’ve been at or near record-low inventory levels for a few years now.

Ready to Hire an Interior Designer?

When hiring an interior designer for your home or business, it’s important to find the right fit. A high-end interior designer can transform your space into a beautiful and functional environment, but finding the right person can be a daunting task. In this article, we’ll discuss some tips on how to hire a high-end interior designer.

Determine Your Budget

The first step in hiring a high-end interior designer is determining your budget. Interior design services can range from a few thousand to several hundred thousand dollars, so it’s important to know what you can afford before beginning your search. Be sure to include a budget for any furnishings, accessories, and materials needed to complete the project.

Research Potential Candidates

Once you have determined your budget, research potential interior designers. Look for designers who specialize in the type of project you are working on, whether a residential or commercial space. Look at their portfolios and read client reviews to get an idea of their style and approach to design. You may also want to ask for referrals from friends or colleagues who have worked with an interior designer in the past.

Schedule Consultations

After you have narrowed down your list of potential candidates, schedule consultations with each. During the consultation, discuss your project goals and budget, and ask the designer about their approach to the project. Be sure to ask about their fees, payment structure, and the timeline for completing the project. It’s important to feel comfortable with the designer you choose, so take note of their communication style and personality during the consultation.

Check References

Before making a final decision, be sure to check the designer’s references. Ask for past clients and contact them about their experience working with the designer. Find out if they were happy with the designer’s work, if the project was completed on time and within budget, and if any issues arose during the project and how they were handled.

Review the Contract

Once you have chosen an interior designer, review the contract carefully before signing. Make sure that all of the project details are included in the contract, including the scope of work, timeline, payment schedule, and any other relevant details. If you have any questions or concerns, discuss them with the designer before signing.

Bottom Line

Hiring a high-end interior designer can be a rewarding experience if done correctly. By determining your budget, researching potential candidates, scheduling consultations, checking references, and reviewing the contract, you can ensure that you find the right designer for your project. With the right designer, you can transform your space into a beautiful and functional environment that meets your needs and exceeds your expectations.

· Houzz – Houzz is a popular website for finding interior designers. They have a directory of designers that you can search based on location, style, and budget. You can also browse photos of past projects to get inspiration for your own space.

· Decorilla – Decorilla is an online interior design service that matches you with a designer who can help you create a custom design plan. They have a team of designers specializing in different styles and budgets, so you can find someone who fits your needs.

· Chairish – Chairish, formerly known as Dering Hall, is an online marketplace for high-end home furnishings and decor, but they also have a directory of interior designers. You can search for designers based on location, style, and project type. They also feature designer portfolios and profiles so you can get a sense of their work.

· A local designer Jennifer has used is Val Valdez

If you’re thinking about buying a home, you might be focusing on previously owned ones. But with so few houses for sale today, it makes sense to consider all your options, and that includes a home that’s newly built.

The Number of Newly Built Homes Is on the Rise

While there are more houses for sale right now than there were at this time last year, there’s still a historically low number of homes available on the market. One reason for that is years of underbuilding—meaning there haven’t been enough new homes built to keep up with demand.

“While existing-home inventory remains limited, the silver lining for home buyers is that new-home inventory is on the rise, and a new home at the right price is a pretty good substitute.”

Builder Incentives Can Provide a Boost

While there a growing number of new homes for sale, builders are slowing that pace until they sell more of their current inventory. According to Logan Mohtashami, Lead Analyst at HousingWire:

“The builders have to work off the backlog of homes, but instead of 3%-4% mortgage rates, they’re dealing with 6% plus mortgage rates, which means they have to provide many incentives to make sure those homes sell.”

Many builders are now offering incentives to help buyers purchase these homes. Fleming also explains:

“The National Association of Home Builders reported that nearly two-thirds of builders were offering incentives, including mortgage rate buydowns, paying points for buyers and price reductions, which could entice potential home buyers.”

A builder who’s willing to pay to reduce your mortgage rate could be a game changer. Ksenia Potapov, Economist at First American, puts it this way:

“A one percentage-point decline in mortgage rates has the same impact on affordability as an 11 percent decline in house prices.”

Should You Buy a Brand-New Home?

The best way to decide what type of home to buy is to work with a trusted real estate professional who can help you weigh the pros and cons of each option. They know which homes are available in your local market, and which builders might be offering incentives that make sense for you.

Bottom Line

Even though there aren’t a lot of homes for sale today, new home inventory is on the rise, and many builders are offering incentives. Let’s connect so I can help you weigh the pros and cons of shopping for a new home versus an existing one.