There’s been a lot of focus on higher mortgage rates and how they’re creating affordability challenges for today’s homebuyers. It’s true that rates climbed dramatically since the record-low we saw during the pandemic. But home affordability is based on more than just mortgage rates – it’s determined by a combination of mortgage rates, home prices, and wages.

Considering how each one of these factors is changing gives you the full picture of home affordability today. Here’s the latest.

1. Mortgage Rates

While mortgage rates are higher than they were a year ago, they’ve hovered primarily between 6% and 7% for nearly eight months now (see graph below):

As the graph shows, mortgage rates have experienced some volatility during that time. And even a small change in mortgage rates impacts your purchasing power. That’s why it’s so important to lean on your team of real estate professionals for expert advice to stay up to date on what’s happening in the market. While it’s hard to project where mortgage rates will go from here, many experts agree they’ll likely continue to remain around 6%-7% in the immediate future.

2. Home Prices

Over the past few years, home prices appreciated rapidly as the record-low mortgage rates we saw during the pandemic led to a surge in buyer demand. The heightened buyer demand happened while the supply of homes for sale was at record lows, and that imbalance put upward pressure on home prices. However, today’s higher mortgage rates have slowed down price appreciation.

And, the truth is, home price appreciation varies by market. Some areas are seeing slight declines while others have prices that are climbing. As Selma Hepp, Chief Economist at CoreLogic, explains:

“The divergence in home price changes across the U.S. reflects a tale of two housing markets. Declines in the West are due to the tech industry slowdown and a severe lack of affordability after decades of undersupply. The consistent gains in the Southeast and South reflect strong job markets, in-migration patterns and relative affordability due to new home construction.”

To find out what’s happening with prices in your local market, reach out to a trusted real estate agent.

3. Wages

The most positive factor in affordability right now is rising income. The graph below uses data from the Bureau of Labor Statistics (BLS) to show how wages have grown over time:

In a seller’s market, it’s not uncommon for homes to sell above their listing price or even their appraised value. But how much is your house worth? Pricing your home correctly is challenging, but there are tools you can use, including hiring an appraiser to complete a pre-appraisal.

A pre-appraisal can be a great jumping off point to identifying the right asking price. With a pre-appraisal in hand, you can work with your real estate agent to assess market conditions and see if you should price higher or lower than the appraised value. You’ll also find insights about your local market on our Home Values page. Simply search by your city, neighborhood, or ZIP code.

Whether you should price your home above its appraisal depends on the accuracy of the appraisal, local market demand, neighborhood appeal and the likelihood you’ll get a cash buyer.

If you sell to a buyer with financing, their lender will order another appraisal before closing to protect themselves from lending more than the house is worth. In that case, it’s ideal to list right at the appraised value, or even a little under, so the deal goes smoothly. But if you have a cash buyer, they’re not beholden to a lender’s appraisal, so they can offer whatever amount they want.

What is a pre-listing home appraisal?

A pre-listing home appraisal is when a professional, licensed local appraiser analyzes your home’s condition in person to determine its value. The appraiser also considers similar homes recently sold in your area. There’s always room for error, as appraisals combine both technical valuations and the appraiser’s professional opinion on what different features of your home are worth.

What an appraisal takes into consideration

Square footage

Number of bedrooms and bathrooms

Age of house

Age of mechanical systems

Condition, layout and finishes

Location and nearby amenities

Comparable recent sales (usually three)

What the appraisal doesn’t cover

Appraisers are looking at the technical and economic aspects of the home and may not account for the human aspect of real estate — buyers will ultimately pay what they think a home is worth, based on how badly they want to buy it. In a sellers market, many buyers are even willing to pay cash to make up the difference between the appraised value and the offer price.

While an appraisal gives you a good idea of your home’s value, there’s no way your appraiser can predict how your home will perform on the open market. Maybe you’ll get 10 offers, and the price will be driven up. Maybe it will stay on the market for weeks or months, and you’ll need to do a price reduction. These are things that no appraiser can account for. If you’re looking for a listing price estimate that weighs all local market factors, review a comparative market analysis (CMA) — more on that later.

Should I get an appraisal before listing?

A pre-appraisal isn’t required, but it can be a good idea if you’ve done a lot of home upgrades recently and you’re not sure how much value they’ve added. They’re also helpful if there aren’t good comparable listings in your area or you’re going to sell for sale by owner (FSBO).

If you’re selling in an extreme buyers or sellers market, your home could sell quite a bit above or below your appraised value, so ask your agent if they think doing a pre-appraisal makes sense for you.

Assessed value vs. appraised value vs. fair market value

When determining the best listing price for your home, you may hear three different terms tossed around: assessed value, appraised value and fair market value. It’s important to understand the differences among the three so you can be smart about deciding how to price your home.

Assessed value

The assessed value of a home comes from the local tax assessor’s office, usually on a yearly basis. It’s the figure they use to determine how much you owe in property taxes. Your home’s assessed value is typically much lower than an appraised value or a fair market value, so it should not be used to determine listing price.

Appraised value

The appraised value is the number your professional licensed appraiser gives you after evaluating your home and reviewing comparable sales. For example, let’s say your home is similar to one down the street that recently sold, but you’ve updated the kitchen. You’ll get “credit” for the updates in your kitchen, and that will be calculated into your appraised value.

Fair market value

Your home’s fair market value is the amount a buyer is actually willing to pay for your home. What a buyer decides to offer is based on a variety of factors, including local market and economic conditions, interest rates, demand, employment and their personal attachment to the home.

Many sellers base their listing price off of what they feel is the fair market value, because it’s the most comprehensive pricing strategy. Depending on the state of your market, sellers sometimes price their home a bit under fair market value in hopes of inciting a bidding war that drives the price up.

How do you find your fair market value? Your real estate agent should provide a CMA that weighs the positive and negative features of your home, as well as local market trends and demand.

What is the average cost of a house appraisal?

You can expect to spend roughly $500 for an appraisal, but the cost can be lower or higher based on where you live and the size of your home.

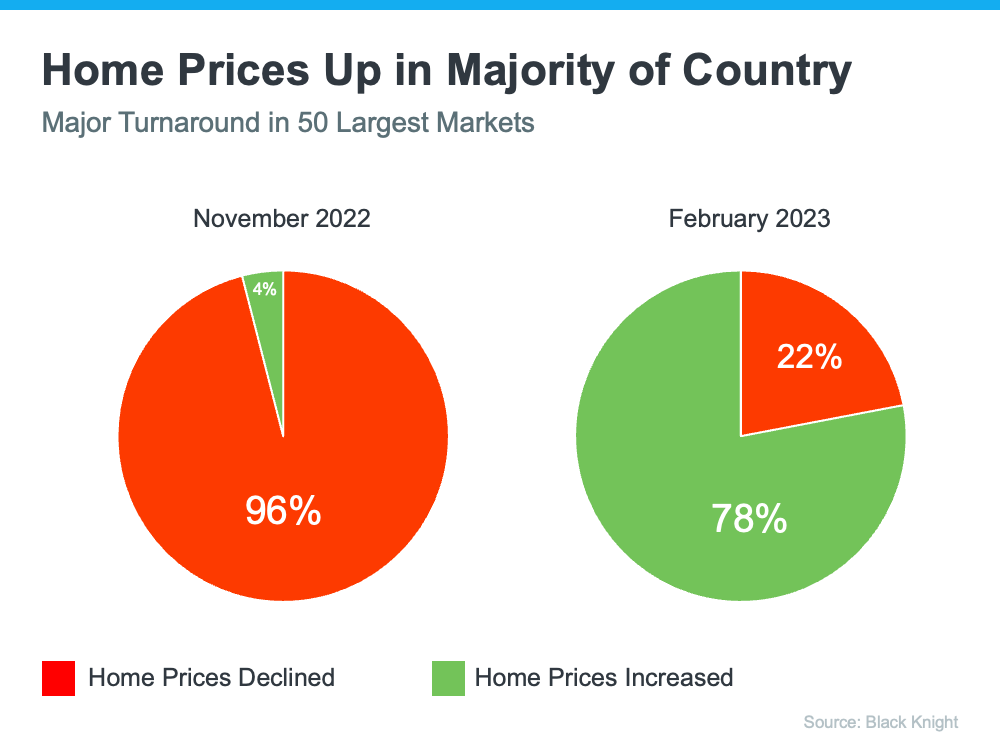

As the housing market continues to change, you may be wondering where it’ll go from here. One factor you’re probably thinking about is home prices, which have come down a bit since they peaked last June. And you’ve likely heard something in the news or on social media about a price crash on the horizon. As a result, you may be holding off on buying a home until prices drop significantly. But that’s not the best strategy.

A recent survey from Zonda shows 53% of millennials are still renting right now because they’re waiting for home prices to come down. But here’s the thing: the most recent data shows that home prices appear to have bottomed out and are now on the rise again. Selma Hepp, Chief Economist at CoreLogic, reports:

“U.S. home prices rose by 0.8% in February . . . indicating that prices in most markets have already bottomed out.”

And the latest data from Black Knight shows the same shift. The graph below compares home price trends in November to those in February:

If you’re thinking about buying a home, you might be focusing on previously owned ones. But with so few houses for sale today, it makes sense to consider all your options, and that includes a home that’s newly built.

The Number of Newly Built Homes Is on the Rise

While there are more houses for sale right now than there were at this time last year, there’s still a historically low number of homes available on the market. One reason for that is years of underbuilding—meaning there haven’t been enough new homes built to keep up with demand.

“While existing-home inventory remains limited, the silver lining for home buyers is that new-home inventory is on the rise, and a new home at the right price is a pretty good substitute.”

Builder Incentives Can Provide a Boost

While there a growing number of new homes for sale, builders are slowing that pace until they sell more of their current inventory. According to Logan Mohtashami, Lead Analyst at HousingWire:

“The builders have to work off the backlog of homes, but instead of 3%-4% mortgage rates, they’re dealing with 6% plus mortgage rates, which means they have to provide many incentives to make sure those homes sell.”

Many builders are now offering incentives to help buyers purchase these homes. Fleming also explains:

“The National Association of Home Builders reported that nearly two-thirds of builders were offering incentives, including mortgage rate buydowns, paying points for buyers and price reductions, which could entice potential home buyers.”

A builder who’s willing to pay to reduce your mortgage rate could be a game changer. Ksenia Potapov, Economist at First American, puts it this way:

“A one percentage-point decline in mortgage rates has the same impact on affordability as an 11 percent decline in house prices.”

Should You Buy a Brand-New Home?

The best way to decide what type of home to buy is to work with a trusted real estate professional who can help you weigh the pros and cons of each option. They know which homes are available in your local market, and which builders might be offering incentives that make sense for you.

Bottom Line

Even though there aren’t a lot of homes for sale today, new home inventory is on the rise, and many builders are offering incentives. Let’s connect so I can help you weigh the pros and cons of shopping for a new home versus an existing one.

If you’re thinking about making a move this year, a turnaround in the housing market could be exactly what you’ve been waiting for. Let’s connect to talk about the latest trends in our area.

![Key Terms To Know When Buying a Home [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2023/01/11164544/Key-Terms-To-Know-When-Buying-A-Home-MEM-1046x2684.png)

There are many people thinking about buying a home, but with everything affecting the economy, some are wondering if it’s a smart decision to buy now or if it makes more sense to wait it out. As Bob Broeksmit, President and CEO of the Mortgage Bankers Association (MBA), explains:

“The desire for homeownership is strong. Many prospective buyers are waiting for the volatility in mortgage rates to subside, as well as for a clearer picture of the economic outlook.”

If you’re in that position, remember that it’s important to consider not just what’s happening today but also what benefits you may gain in the long run.

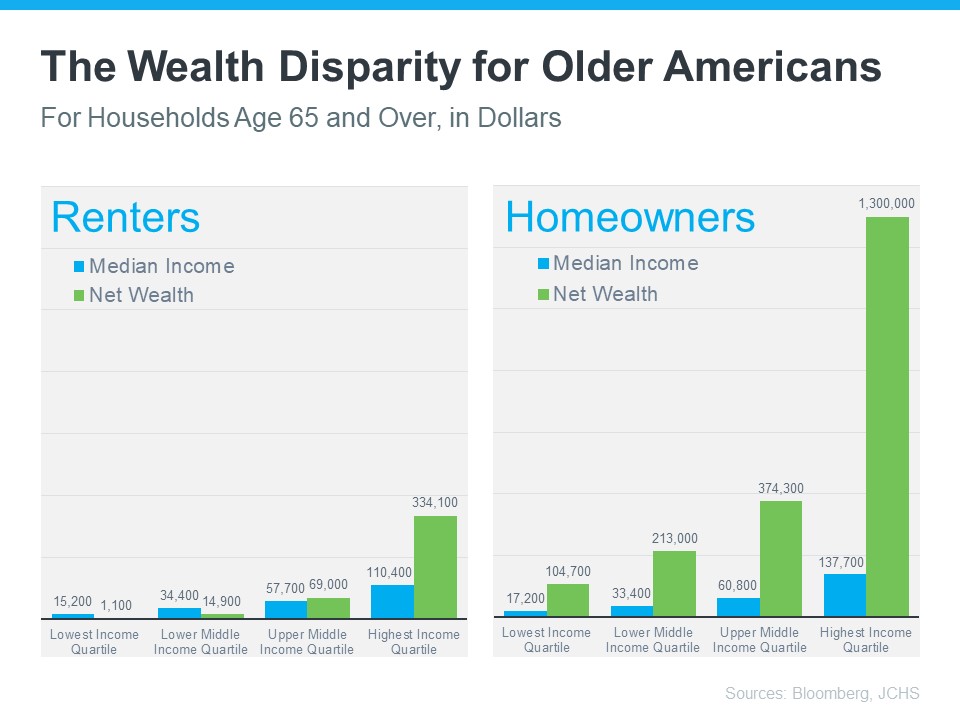

There’s a lot of information out there about how homeownership helps build a homeowner’s net worth over time. But even today, many people think first about things like 401(k)s before they think of owning a home as a wealth-building tool. It’s especially important if you’re a young prospective homebuyer to understand how homeownership is another key way to invest in your future. An article from Bloomberg notes:

“Millennials have higher average 401(k) balances than Generation X did when they were the same age, but they’re not any better off financially. . . . A lot of that has to do with being less likely to own a home.”

To help you understand just how much owning a home can have a positive impact on your life over the years, take a look at what the data shows. The same Bloomberg article helps show the gap in wealth between renters and homeowners who are 65 years and older (see graph below). The difference is substantial, even when incomes are similar.

So, if you want to create wealth to help set you up for success later on, it may be time to prioritize homeownership. That’s because, whether you decide to rent or buy a home, you’ll have a monthly housing expense either way. The question is: are you going to invest in yourself and your future, or will you help someone else (your landlord) increase their wealth?

Before putting your homeownership plans on hold, let’s connect to go over your options. That way, you’ll have expert advice on how to make the best decision right now and the best investment in your future.