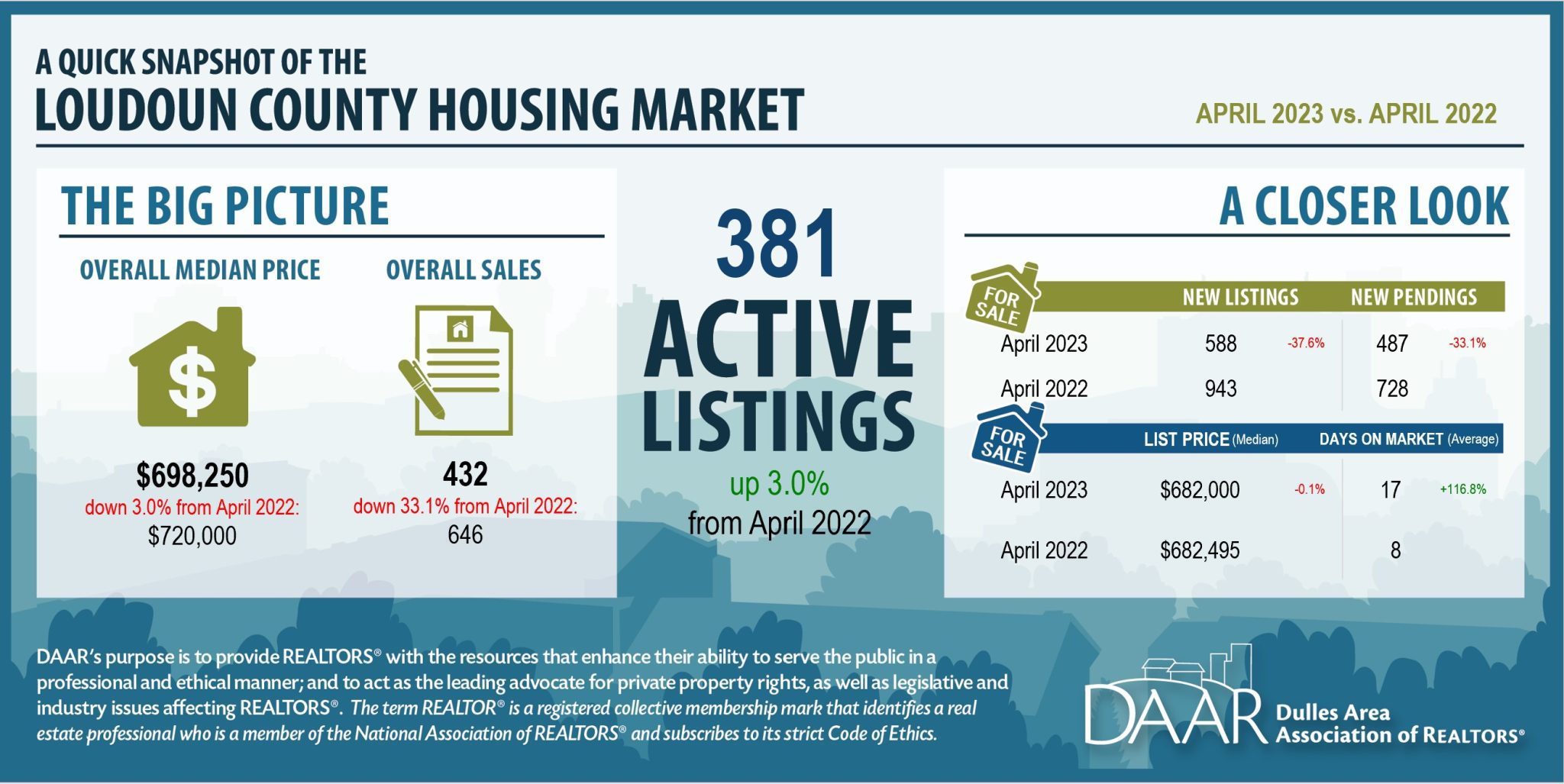

Key Market Trends

Sales activity remains well below last year’s level across most local markets in Loudoun County.

There were 432 sales countywide this month, 214 fewer sales than last April, a 33.1% drop off in activity. This is the slowest April market the county has had in more than a decade. Ashburn zip code 20148 had the biggest decrease in sales with 33 fewer sales than last year (-30.8%) while sales in Leesburg zip code 20176 declined by 21 sales (-29.2%). The only market where sales increased was Lovettsville 20180 with seven more sales than the previous year (+63.6%).

Pending sales cool, signaling a continuation of the slow spring market.

There were 487 pending sales in April in Loudoun County, 241 fewer pending sales than the same time a year ago, falling by 33.1%. Pending sales dipped the most in Ashburn zip code 20147 with 41 fewer pending sales (-34.2%) and Aldie zip code 20105 with 35 fewer pending sales than last year (-51.5%).

The median sales price in the Loudoun County housing market dipped from last April.

In April, the median sales price countywide was $698,250, a 3% decrease in price, which is $21,750 less than last year. This is only the second time in the last four years that the monthly median sales price was lower than the prior year. The sharpest price drops occurred in Lovettsville zip code 20180 down $135,000 from a year ago (-16.3%), Leesburg zip code 20175 (-12.2%) and Chantilly zip code 20152 (-11.1%). In Aldie zip code 20105, home prices were up $45,000 or 5.4%.

The number of active listings continues to build up in most parts of the county.

There were 381 active listings at the end of April in Loudoun County, 11 more listings than the year prior, a 3% increase. In Sterling zip code 20164 there were 13 more listings on the market than last year (+56.5%). Listings fell in Chantilly zip code 20152 with nine fewer listings than the previous year (-52.9%). The total number of new listings in Loudoun County plunged by 37.6% compared to last April.

Data Note: The housing market data for all jurisdictions in Virginia was re-benchmarked in November 2021. Please note that Market Indicator Reports released prior to November 2021 were produced using the prior data vintage and may not tie to reports that use the current data set for some metrics. We recommend using the current reports for historical comparative analysis.

If you’re reading headlines about inflation or mortgage rates, you may see something about the recent decision from the Federal Reserve (the Fed). But what does it mean for you, the housing market, and your plans to buy a home? Here’s what you need to know.

Inflation and the Housing Market

While the Fed’s working hard to lower inflation, the latest data shows that, while the number has improved some, the inflation rate is still higher than the target (2%). That played a role in the Fed’s decision to raise the Federal Funds Rate last week. As Bankrate explains:

“Keeping its inflation-fighting streak alive, the Federal Reserve has raised interest rates for the 10th time in 10 meetings . . . The hikes aimed to cool an economy that was on fire after rebounding from the coronavirus recession of 2020.”

While the Fed’s actions don’t directly dictate what happens with mortgage rates, their decisions do have an impact and contributed to the intentional cooldown in the housing market last year.

How This Impacts You

During times of high inflation, your everyday expenses go up. That means you’ve likely felt the pinch at the gas pump and in the grocery store. By raising the Federal Funds Rate, the Fed is actively trying to lower inflation. If the Fed is successful, it could also ultimately lead to lower mortgage rates and better homebuying affordability for you. That’s because when inflation is high, mortgage rates tend to be high. But, as inflation cools, experts say mortgage rates will likely fall.

Where Experts Think Mortgage Rates and Inflation Will Go from Here

Moving forward, both inflation and mortgage rates will continue to impact the housing market. And as Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Mortgage rates are likely to descend lower later in the year as the consumer price inflation calms down . . .”

Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), explains:

“We continue to expect that mortgage rates will drift down over the course of the year as the economy slows . . .”

While there’s no way to say with certainty where mortgage rates will go from here, the experts think mortgage rates will trend down this year if inflation comes down too. To stay informed on the latest insights, connect with a trusted real estate advisor. They keep their pulse on what’s happening today and help you understand what the experts are projecting and how it could impact your homeownership plans.

Bottom Line

Don’t let headlines about the latest decision from the Fed confuse you. Where mortgage rates go from here depends on what happens with inflation. If inflation cools, mortgage rates should tick down as a result. Let’s connect so you have expert insights on housing market changes and what they mean for you.

How Bridge Loans Can Help You Purchase

Bridge loans are a great financial tool to provide you

with the flexibility to make a non-contingent offer, leverage the equity in

your current home without having to do a simultaneous close/move, and/or

qualify for a purchase prior to selling your departing property.

The most common type of bridge loan is a current (departing)

property bridge loan which pulls equity out of your current primary residence

to be used for the down payment on a new home or to purchase your new home in

cash.

A bridge loan can also be used on the property you are purchasing.

One benefit of a purchase bridge loan is that if certain conditions are met

(departing residence listed for sale and available reserves) then the monthly

payment associated with the departing residence may be excluded from the DTI calculation.

This allows a borrower who doesn’t qualify carrying both homes

to purchase their new home prior to selling their departing residence.

A bridge loan can be used on both the departing residence

and the purchase property when the borrower needs both the equity from the

current property yet does not qualify carrying both properties.

Atlantic Coast Mortgage bridge loans are 6-month interest only with no

escrows and are allowed on primary residences or second homes in DC, MD, NC,

VA, and Charleston, SC MSA. The bridge loan will take first lien position so any existing mortgages will be paid off in addition any proceeds received.

For further information please reach out to Melissa Bell, NMLS ID 450558, with Atlantic Coast Mortgage.

Atlantic Coast Mortgage, LLC is an Equal Housing Lender

Everywhere you look, people are talking about a potential recession. And if you’re planning to buy or sell a house, this may leave you wondering if your plans are still a wise move. To help ease your mind, experts are saying that if we do officially enter a recession, it’ll be mild and short. As the Federal Reserve explained in their March meeting:

“. . . the staff’s projection at the time of the March meeting included a mild recession starting later this year, with a recovery over the subsequent two years.”

While a recession may be on the horizon, it won’t be one for the housing market record books like the crash in 2008. What we have to remember is that a recession doesn’t always lead to a housing crisis.

To prove it, let’s look at the historical data of what happened in real estate during previous recessions. That way you know why you shouldn’t be afraid of what a recession could mean for the housing market today.

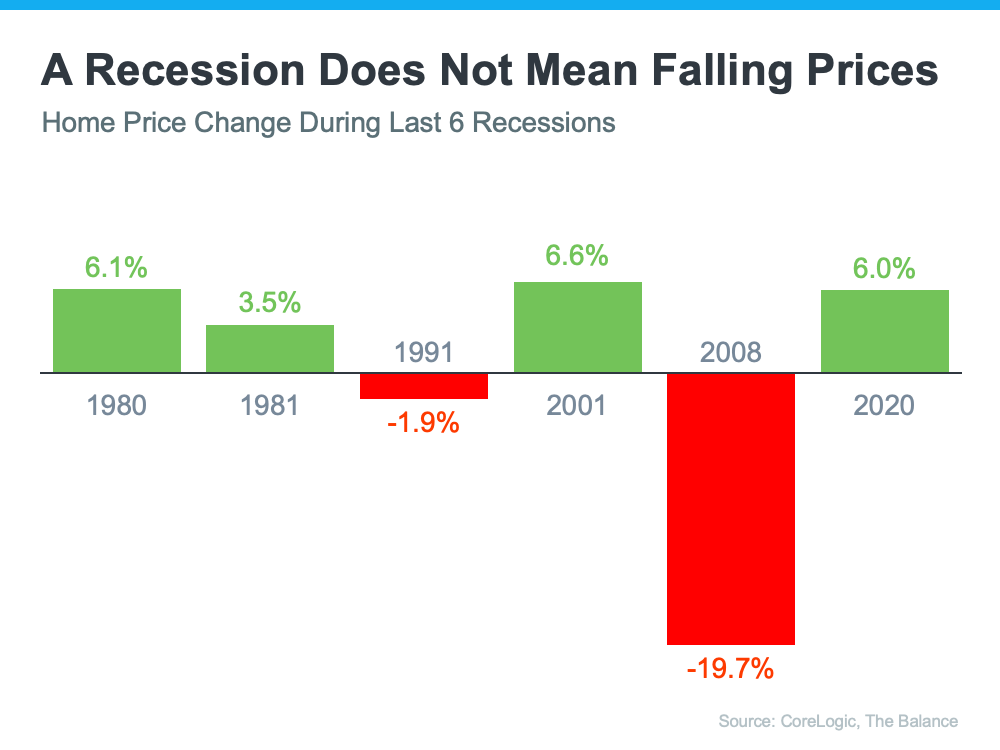

A Recession Doesn’t Mean Falling Home Prices

To show that home prices don’t fall every time there’s a recession, it helps to turn to historical data. As the graph below illustrates, looking at recessions going all the way back to 1980, home prices appreciated in four of the last six of them. So historically, when the economy slows down, it doesn’t mean home values will always fall.

Most people remember the housing crisis in 2008 (the larger of the two red bars in the graph above) and think another recession will be a repeat of what happened to housing then. But today’s housing market isn’t about to crash because the fundamentals of the market are different than they were in 2008. Back then, one of the big reasons why prices fell was because there was a surplus of homes for sale at the same time distressed properties flooded the market. Today, the number of homes for sale is low, so while home prices may see slight declines in some areas and slight gains in others, a crash simply isn’t in the cards.

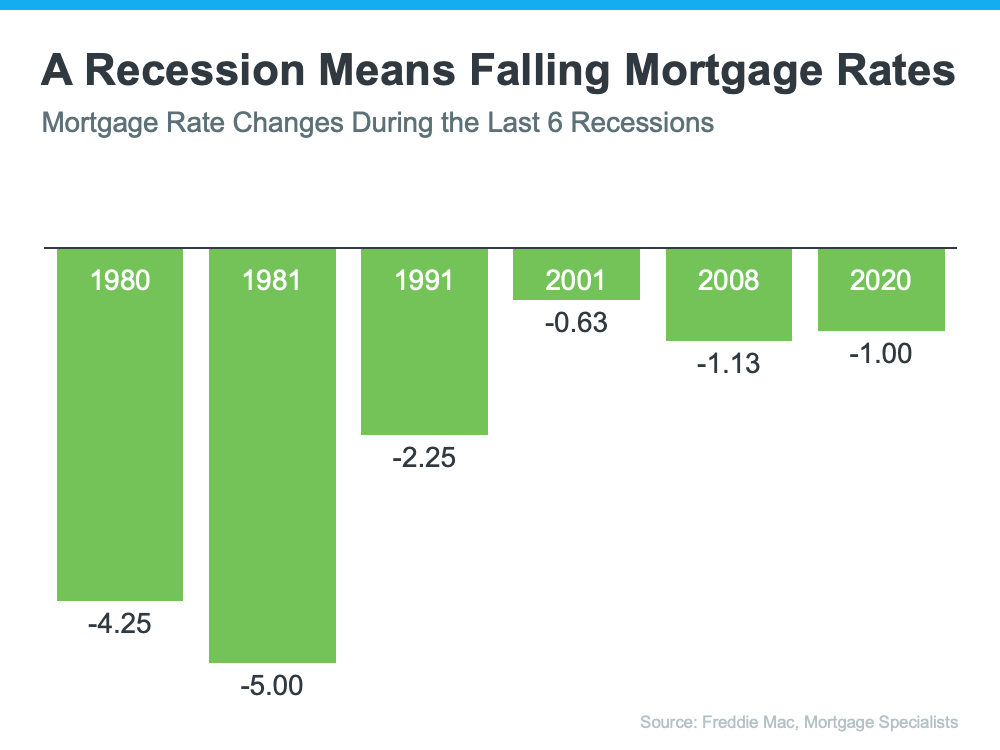

A Recession Means Falling Mortgage Rates

What a recession really means for the housing market is falling mortgage rates. As the graph below shows, historically, each time the economy slowed down, mortgage rates decreased.

There’s been a lot of focus on higher mortgage rates and how they’re creating affordability challenges for today’s homebuyers. It’s true that rates climbed dramatically since the record-low we saw during the pandemic. But home affordability is based on more than just mortgage rates – it’s determined by a combination of mortgage rates, home prices, and wages.

Considering how each one of these factors is changing gives you the full picture of home affordability today. Here’s the latest.

1. Mortgage Rates

While mortgage rates are higher than they were a year ago, they’ve hovered primarily between 6% and 7% for nearly eight months now (see graph below):

As the graph shows, mortgage rates have experienced some volatility during that time. And even a small change in mortgage rates impacts your purchasing power. That’s why it’s so important to lean on your team of real estate professionals for expert advice to stay up to date on what’s happening in the market. While it’s hard to project where mortgage rates will go from here, many experts agree they’ll likely continue to remain around 6%-7% in the immediate future.

2. Home Prices

Over the past few years, home prices appreciated rapidly as the record-low mortgage rates we saw during the pandemic led to a surge in buyer demand. The heightened buyer demand happened while the supply of homes for sale was at record lows, and that imbalance put upward pressure on home prices. However, today’s higher mortgage rates have slowed down price appreciation.

And, the truth is, home price appreciation varies by market. Some areas are seeing slight declines while others have prices that are climbing. As Selma Hepp, Chief Economist at CoreLogic, explains:

“The divergence in home price changes across the U.S. reflects a tale of two housing markets. Declines in the West are due to the tech industry slowdown and a severe lack of affordability after decades of undersupply. The consistent gains in the Southeast and South reflect strong job markets, in-migration patterns and relative affordability due to new home construction.”

To find out what’s happening with prices in your local market, reach out to a trusted real estate agent.

3. Wages

The most positive factor in affordability right now is rising income. The graph below uses data from the Bureau of Labor Statistics (BLS) to show how wages have grown over time:

The Power of Pre-Approval

If you’re buying a home this spring, today’s housing market can feel like a challenge. With so few homes on the market right now, plus higher mortgage rates, it’s essential to have a firm grasp on your homebuying budget. You’ll also need a sense of determination to find the right house and act quickly when you go to put in an offer. One thing you can do to help you prepare is to get pre-approved.

To understand why it’s such an important step, you need to know what pre-approval is. As part of the process, a lender looks at your finances to determine what they’d be willing to loan you. From there, your lender will give you a pre-approval letter to help you understand how much money you can borrow.

Freddie Mac explains it like this:

“A pre-approval is an indication from your lender that they are willing to lend you a certain amount of money to buy your future home. . . . Keep in mind that the loan amount in the pre-approval letter is the lender’s maximum offer. Ultimately, you should only borrow an amount you are comfortable repaying.”

Basically, pre-approval gives you critical information about the homebuying process that’ll help you understand how much you may be able to borrow so you have a stronger grasp of your options. And with higher mortgage rates impacting affordability for many buyers today, a solid understanding of your numbers is even more important.

Pre-Approval Helps Show You’re a Serious Buyer

That’s not the only thing pre-approval can do. Another added benefit is it can help a seller feel more confident in your offer because it shows you’re serious about buying their house. And, with sellers seeing a slight increase in the number of offers again this spring, making a strong offer when you find the perfect house is key.

As a recent article from the Wall Street Journal (WSJ) says:

“If you plan to use a mortgage for your home purchase, preapproval should be among the first steps in your search process. Not only can getting preapproved help you zero in on the right price range, but it can give you a leg up on other buyers, too.”

Bottom Line

Getting pre-approved is an important first step when you’re buying a home. It lets you know what you can borrow for your loan and shows sellers you’re serious. Connect with a local real estate professional and a trusted lender so you have the tools you need to purchase a home in today’s market.

Loudoun County Key Market Trends

March 2023

Sales activity continues to moderate in Loudoun County.

There were 376 sales in the county during the month of March, 203 fewer sales than last year, a 35.1% decrease. The markets where sales declined the most were in Ashburn zip code 20148 with 48 fewer sales (-49.5%) and Leesburg zip code 20176 down 28 sales from a year ago (-42.4%). Sterling zip code 20164 saw sales go up this month with 6 more sales than last March (+18.2%).

Pending sales activity continues to be sluggish.

In March, there were 461 pending sales across the county, 192 fewer pending sales than the previous year, a 29.4% drop off. Ashburn zip code 20148 had 29 fewer pending sales (-28.2%) and Chantilly zip code 20152 was down 24 pending sales from the year prior (-46.2%). Lovettsville zip code 20180 was the only local market in the county to have an uptick in pending sales this month (+50.0%), 6 additional pending sales compared to last March.

Home prices continue to climb in most local markets in the county.

The countywide median sales price in March was $720,000, up 5.9% from a year ago, an increase of $40,000. Median prices saw the biggest growth in Aldie zip code 20105 up $215,000 (+29.5%) and in Leesburg zip code 20176 with a gain of $187,500 from last year (+31.4%). The biggest price drops happened in Purcellville zip code 20132 (-11.3%) and Sterling zip code 20165 (-5.3%).

The number of active listings is building up in Loudoun County even as fewer new listings are coming on the market.

In the Loudoun County housing market, there were 355 active listings at the end of March, 98 more listings than a year ago, a 38.1% increase. Ashburn zip code 20147 experienced the sharpest rise in listings with 29 more listings (+131.8%) followed by Leesburg zip code 20176 with 26 additional listings (+136.8%). There were 627 new listings in March across the county, 211 fewer new listings than this time last year (-25.2%).

Data Note: The housing market data for all jurisdictions in Virginia was re-benchmarked in November 2021. Please note that Market Indicator Reports released prior to November 2021 were produced using the prior data vintage and may not tie to reports that use the current data set for some metrics. We recommend using the current reports for historical comparative analysis.

Falling out of Love with Your House? It May Be Time To Move.

Owning a home means having a place that’s solely your own and provides the space, features, and location you and your loved ones need. But what happens when your needs change? If this hits home for you, it may be time to make a move.

According to the latest Home Buyers and Sellers Generational Trends Report from the National Association of Realtors (NAR), the average person has lived in their current house for ten years. If you’ve been in your home for a while, think about how much in your life has changed since you moved in. Even if you thought it would be your forever home when you bought it, it doesn’t have to be. Work with a local real estate agent to explore all your options in today’s market before settling for your current home.

That’s actually what a lot of homeowners are doing right now. A recent survey from Realtor.com finds that, of people who are considering selling in 2023, one in three are thinking about moving because their home no longer meets their needs. And according to the same report from NAR, that’s consistent with this year’s top reasons for selling, which include:

If things in your life have changed, it may be time to make a move. And there’s good news: it’s still a great time to sell. Here’s why.

We’re in a strong sellers’ market. That means homes listed at market value and in good condition are getting attention from buyers and selling quickly. Lean on your expert real estate advisor for the best advice on getting your house ready to sell.

Your equity can power your next move. There’s a good chance you have a significant amount of equity right now thanks to record levels of price appreciation in recent years. When you sell, you can use that equity to help afford your next home. In fact, NAR’s report from above shows 38% of recent buyers used the money from the sale of their previous home to cover the down payment on their next one. Work with a local real estate agent to learn how much equity you have and what you can do with it in today’s housing market.

Bottom Line

If your home no longer meets your needs, consider selling it so you can find your dream home. Let’s connect so you can learn about your options.

In a seller’s market, it’s not uncommon for homes to sell above their listing price or even their appraised value. But how much is your house worth? Pricing your home correctly is challenging, but there are tools you can use, including hiring an appraiser to complete a pre-appraisal.

A pre-appraisal can be a great jumping off point to identifying the right asking price. With a pre-appraisal in hand, you can work with your real estate agent to assess market conditions and see if you should price higher or lower than the appraised value. You’ll also find insights about your local market on our Home Values page. Simply search by your city, neighborhood, or ZIP code.

Whether you should price your home above its appraisal depends on the accuracy of the appraisal, local market demand, neighborhood appeal and the likelihood you’ll get a cash buyer.

If you sell to a buyer with financing, their lender will order another appraisal before closing to protect themselves from lending more than the house is worth. In that case, it’s ideal to list right at the appraised value, or even a little under, so the deal goes smoothly. But if you have a cash buyer, they’re not beholden to a lender’s appraisal, so they can offer whatever amount they want.

What is a pre-listing home appraisal?

A pre-listing home appraisal is when a professional, licensed local appraiser analyzes your home’s condition in person to determine its value. The appraiser also considers similar homes recently sold in your area. There’s always room for error, as appraisals combine both technical valuations and the appraiser’s professional opinion on what different features of your home are worth.

What an appraisal takes into consideration

Square footage

Number of bedrooms and bathrooms

Age of house

Age of mechanical systems

Condition, layout and finishes

Location and nearby amenities

Comparable recent sales (usually three)

What the appraisal doesn’t cover

Appraisers are looking at the technical and economic aspects of the home and may not account for the human aspect of real estate — buyers will ultimately pay what they think a home is worth, based on how badly they want to buy it. In a sellers market, many buyers are even willing to pay cash to make up the difference between the appraised value and the offer price.

While an appraisal gives you a good idea of your home’s value, there’s no way your appraiser can predict how your home will perform on the open market. Maybe you’ll get 10 offers, and the price will be driven up. Maybe it will stay on the market for weeks or months, and you’ll need to do a price reduction. These are things that no appraiser can account for. If you’re looking for a listing price estimate that weighs all local market factors, review a comparative market analysis (CMA) — more on that later.

Should I get an appraisal before listing?

A pre-appraisal isn’t required, but it can be a good idea if you’ve done a lot of home upgrades recently and you’re not sure how much value they’ve added. They’re also helpful if there aren’t good comparable listings in your area or you’re going to sell for sale by owner (FSBO).

If you’re selling in an extreme buyers or sellers market, your home could sell quite a bit above or below your appraised value, so ask your agent if they think doing a pre-appraisal makes sense for you.

Assessed value vs. appraised value vs. fair market value

When determining the best listing price for your home, you may hear three different terms tossed around: assessed value, appraised value and fair market value. It’s important to understand the differences among the three so you can be smart about deciding how to price your home.

Assessed value

The assessed value of a home comes from the local tax assessor’s office, usually on a yearly basis. It’s the figure they use to determine how much you owe in property taxes. Your home’s assessed value is typically much lower than an appraised value or a fair market value, so it should not be used to determine listing price.

Appraised value

The appraised value is the number your professional licensed appraiser gives you after evaluating your home and reviewing comparable sales. For example, let’s say your home is similar to one down the street that recently sold, but you’ve updated the kitchen. You’ll get “credit” for the updates in your kitchen, and that will be calculated into your appraised value.

Fair market value

Your home’s fair market value is the amount a buyer is actually willing to pay for your home. What a buyer decides to offer is based on a variety of factors, including local market and economic conditions, interest rates, demand, employment and their personal attachment to the home.

Many sellers base their listing price off of what they feel is the fair market value, because it’s the most comprehensive pricing strategy. Depending on the state of your market, sellers sometimes price their home a bit under fair market value in hopes of inciting a bidding war that drives the price up.

How do you find your fair market value? Your real estate agent should provide a CMA that weighs the positive and negative features of your home, as well as local market trends and demand.

What is the average cost of a house appraisal?

You can expect to spend roughly $500 for an appraisal, but the cost can be lower or higher based on where you live and the size of your home.