WASHINGTON (December 13, 2022) – Lawrence Yun, National Association of Realtors (NAR) chief economist and senior vice president of research, forecasts that 4.78 million existing homes will be sold, prices will remain stable, and Atlanta will be the top real estate market to watch in 2023 and beyond. Yun unveiled the association’s forecast today during NAR’s fourth annual year-end Real Estate Forecast Summit.

Yun predicts home sales will decline by 6.8% compared to 2022 (5.13 million) and the median home price will reach $385,800 – an increase of just 0.3% from this year ($384,500).

“Half of the country may experience small price gains, while the other half may see slight price declines,” Yun said. “However, markets in California may be the exception, with San Francisco, for example, likely to register price drops of 10–15%.”

Yun expects rent prices to rise 5% in 2023, following a 7% increase in 2022. He predicts foreclosure rates will remain at historically low levels in 2023, comprising less than 1% of all mortgages.

Yun forecasts U.S. GDP will grow by 1.3%, roughly half the typical historical pace of 2.5%. After eclipsing 7% in late 2022, he expects the 30-year fixed mortgage rate to settle at 5.7% as the Fed slows the pace of rate hikes to control inflation. Yun noted this is lower than the pre-pandemic historical rate of 8%.

NAR identified 10 real estate markets that it expects to outperform other metro areas in 2023. In order the markets are as follows:

“The demand for housing continues to outpace supply,” Yun said. “The economic conditions in place in the top 10 U.S. markets, all of which are located in the South, provide the support for home prices to climb by at least 5% in 2023.”

NAR selected the top 10 real estate markets to watch in 2023 based on how they compared to the national average on the following economic indicators: 1) better housing affordability; 2) greater numbers of renters who can afford to buy a median-priced home; 3) stronger job growth; 4) faster growth of information industry jobs; 5) higher shares of the information industry in the respective local GDPs; 6) migration gains; 7) shares of workers teleworking; 8) faster population growth; 9) faster growth of active housing inventory; and 10) smaller housing shortages.

To view NAR’s On the Horizon: Markets to Watch in 2023 and Beyond report, visit this page.

The National Association of Realtors® is America’s largest trade association, representing more than 1.5 million members involved in all aspects of the residential and commercial real estate industries.

*originally posted on RETechnology 12/15/22

![2023 Housing Market Forecast [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/12/15125347/2023-Housing-Market-Forecast-MEM-1046x2665.png)

Did the frequency and intensity of bidding wars over the past two years make you put your home search on hold? If so, you should know the hyper competitive market has cooled this year as buyer demand has moderated and housing supply has grown. Those two factors combined mean you may see less competition from other buyers.

And with less competition comes more opportunity. Here are two trends that may be the news you need to reenter the market.

Over the last two years, more buyers were willing to skip important steps in the homebuying process, like the appraisal or the inspection, in hopes of gaining an advantage in a bidding war. But now, things are different.

The latest data from the National Association of Realtors (NAR) shows the percentage of buyers waiving their home inspection or appraisal is down. And a recent article from realtor.com points out more sellers are accepting contingencies:

“A year ago, sellers were calling all the shots and buyers were launching legendary bidding wars, waiving contingencies, and paying for homes in cash. But now, the shoe is on the other foot, and 92% of home sellers are accepting some buyer-friendly terms (frequently related to home inspections, financing, or appraisals), . . .”

This doesn’t mean we’re in a buyers’ market now, but it does mean you have a bit more leverage when it comes time to negotiate with a seller. The days of feeling like you may need to waive contingencies or pay drastically over asking price to get your offer considered may be coming to a close.

Before the pandemic, it was a common negotiation tactic for sellers to cover some of the buyer’s closing costs to sweeten the deal. This didn’t happen as much during the peak buyer frenzy over the past two years.

Today, data suggests this is making a comeback. A realtor.com survey shows 32% of sellers paid some or all of their buyer’s closing costs. This may be a negotiation tool you’ll see as you go to purchase a home. Just keep in mind, limits on closing cost credits are set by your lender and can vary by state and loan type. Work closely with your loan advisor to understand how much a seller can contribute to closing costs in your area.

Despite the extremely competitive housing market of the past several years, today’s data suggests negotiations are starting to come back to the table. To find out how the market is shifting in our area, let’s connect today.

![Reasons To Sell Your House This Season [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/12/08121045/Reasons-To-Sell-Your-House-This-Season-MEM-1046x2601.png)

There are many people thinking about buying a home, but with everything affecting the economy, some are wondering if it’s a smart decision to buy now or if it makes more sense to wait it out. As Bob Broeksmit, President and CEO of the Mortgage Bankers Association (MBA), explains:

“The desire for homeownership is strong. Many prospective buyers are waiting for the volatility in mortgage rates to subside, as well as for a clearer picture of the economic outlook.”

If you’re in that position, remember that it’s important to consider not just what’s happening today but also what benefits you may gain in the long run.

There’s a lot of information out there about how homeownership helps build a homeowner’s net worth over time. But even today, many people think first about things like 401(k)s before they think of owning a home as a wealth-building tool. It’s especially important if you’re a young prospective homebuyer to understand how homeownership is another key way to invest in your future. An article from Bloomberg notes:

“Millennials have higher average 401(k) balances than Generation X did when they were the same age, but they’re not any better off financially. . . . A lot of that has to do with being less likely to own a home.”

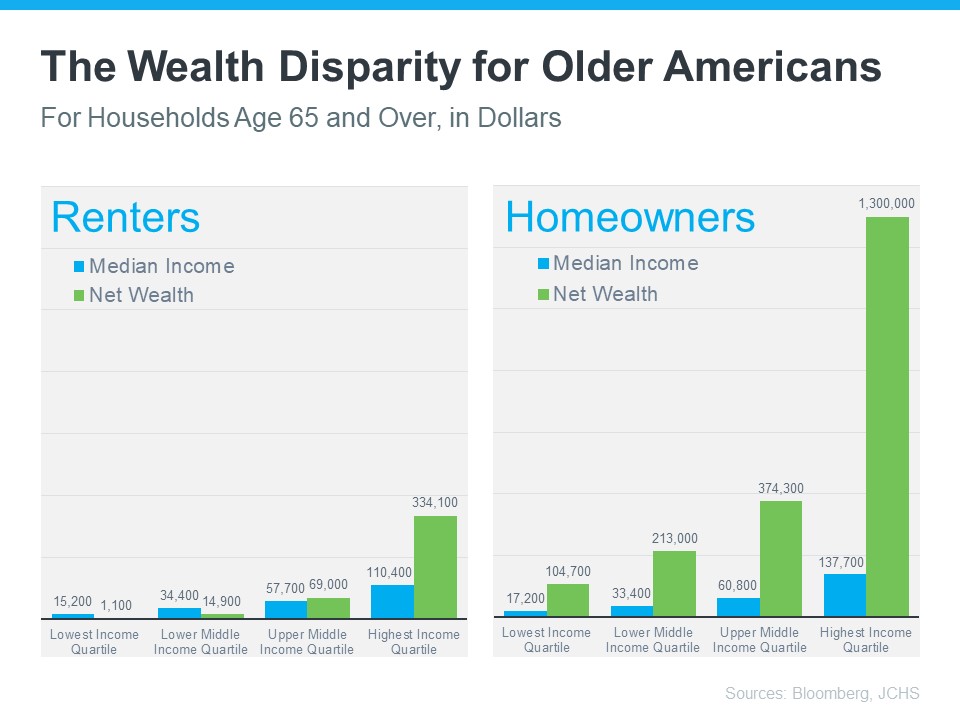

To help you understand just how much owning a home can have a positive impact on your life over the years, take a look at what the data shows. The same Bloomberg article helps show the gap in wealth between renters and homeowners who are 65 years and older (see graph below). The difference is substantial, even when incomes are similar.

So, if you want to create wealth to help set you up for success later on, it may be time to prioritize homeownership. That’s because, whether you decide to rent or buy a home, you’ll have a monthly housing expense either way. The question is: are you going to invest in yourself and your future, or will you help someone else (your landlord) increase their wealth?

Before putting your homeownership plans on hold, let’s connect to go over your options. That way, you’ll have expert advice on how to make the best decision right now and the best investment in your future.